You Can't Always Get What You Want

- Scott Poore

- Jan 16

- 5 min read

Sometimes investors are their own worst enemies. Just when things are going well, they

seem to wish for calamity. Stocks are up to start the year, inflation is under control, and unemployment is steady. That doesn't seem to be enough for some investors. The inspiration for this week's musings is the 1969 hit song, "You Can't Always Get What You Want" by the Rolling Stones. Here’s some trivia about the song:

This song did not actually chart on the Billboard charts in 1969 - yes, you heard that correctly. Despite being named to Rolling Stone Magazine's top 500 songs of all time, it didn't even register in 1969. Why? It was released as the B side (that's a vinyl record for those born in the era of CDs and digital music) to "Honky Tonk Women." That song was a No. 1 hit in 1969, while "You Can't Always Get What You Want" received little promotion or radio play.

The song addresses the key issues that dominated the '60s - love, politics, and drugs. However, the inspiration for the song is debated. According to some, the song is an homage to a man named Jimmy Hutmaker, a local character who wandered the business district in Excelsior, Minnesota where the Stones performed their first U.S. tour in 1964. In the third set of verses of the song, it mentions "I was standing in line with Mr. Jimmy, And man, did he look pretty ill, We decided that we would have a soda, My favourite flavour, cherry red, I sung my song to Mr. Jimmy." Hutmaker claims to have been standing in line to get a drink at the local drug store. The store didn't have the drink of Mick Jagger's choice, to which Mr. Hutmaker replied, "Well, you can't always get what you want."

Still, others claim the reference to a drug store is frivolous and that Mr. Jimmy is a homage to Jimmy Miller, who was the Stones producer at the time. According to Jagger, Stones drummer Charlie Watts had trouble playing the "groove" so Jimmy Miller had to play the drums on the recording. You be the judge.

The London Bach Choir sings at the beginning of the song. Their 60 voiced were double-tracked to make it sound like there were even more singing. The Choir tried, unsuccessfully, to remove their names from the album credits when they discovered the album contained "Midnight Rambler" about a serial killer.

"I saw her today at the reception

A glass of wine in her hand

I knew she would meet her connection

At her feet was a foot-loose man

No, you can't always get what you want

You can't always get what you want

You can't always get what you want

But if you try sometime, you'll find

You get what you need"

Here's what we've seen so far this week...

Waiting On The Next Shoe To Drop. As the Stones sang in this song, sometimes you can't find happiness. No matter what you have, you always want more. Well, in the case

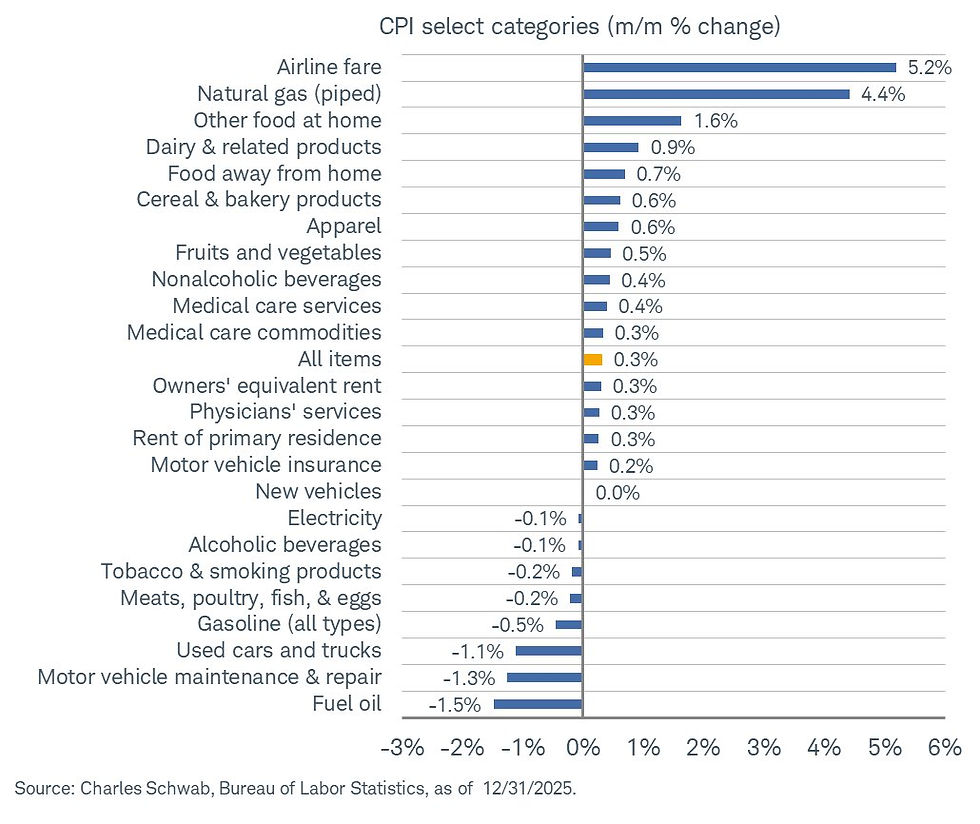

of economists, they can't seem to find happiness, even when the numbers suggest they should. This week the December reading for inflation (CPI) came in as expected, +0.3% for the month, and was unchanged (+2.7%) on a year-over-year basis. As long as inflation remains stable, the door remains open for a rate cut. Current futures show the first possible rate cut in June with an 81% probability of a 25 basis point cut.

The struggle some investors have is understanding the relationship between growth and inflation. In order for the economy to grow, consumers need to spend. When

consumers spend, corporations generate revenues, causing stock prices to rise with better profitability. When this occurs, it means the speed of money (inflation) has increased. Some inflation is good for the economy. Runaway inflation causes consumers to slow spending which is bad for the economy. In December, some key categories that have been elevated, saw some declines. Electricity, Gasoline, Meat, Poultry, Fish, & Eggs all saw declines. In addition, Vehicle Maintenance saw a large drop providing some ease to consumers. If we continue to see a stable inflation environment, that would bode well for the consumer and the economy.

Another struggle for investors is expecting things to get worse. There will come a time when markets under-perform, but why wait around expecting it? Thus is the case with

stagflation. A good reminder that stagflation exists when there is low growth, high unemployment, and rising inflation. The most relevant case study in stagflation occurred from 1973 to 1975. In that period, which included a recession, unemployment spiked from 1% to 25%, while GDP was stalled around 1%, and inflation rose from 2.3% to 3%. Contrast that environment to today, unemployment, while slightly rising has proven relatively stable, inflation has declined from 5% in 2023 to 2.7% in 2025, and GDP is on the rise. In fact, the Atlanta Fed increased their GDPNow forecast this week for 4th quarter GDP from +5.1% to +5.3%. As it stands today, there's not much of a case for stagflation. With some discussion of the Fed not lowering rates this year, it would be hard to make a case for stagflation if the Fed is able to sit on the sidelines in 2026 due to a solid economic backdrop.

Sometimes, You Get What You Need. One thing that is needed for equity markets to continue current trends is breadth. Over the past couple of weeks we have seen

breadth improve to levels not seen since 2024. The number of S&P 500 stocks making new highs relative to stocks making new lows is at a 14-month high. In similar fashion, the number of S&P 500 stocks rising above their respective 200-day moving averages is at 70.4%, a number also not seen since 2024. This would indicate that there is a real possibility that sectors other than Technology may lead this year.

Over the last month, the Technology sector has given way to other equity sectors in

terms of leadership. Technology isn't exactly falling apart, up more than 3% over that time frame. However, Energy, Materials, Industrials, Consumer Staples, and Real Estate - all sectors that lagged Tech in 2025 - are out-pacing the momentum sector over the past 4 weeks. We'll see if that trend continues.

Lastly, we need for the trend of discretionary stocks relative to staples to stay in tact in

order for equities to continue to move higher. So far, that remains the case. When the ratio of consumer discretionary stocks to consumer staple stocks moves lower, it means investors are moving to safer areas of the equity market and a downturn in the market should be expected. Right now, the trend of discretionary stocks out-pacing staples that started in October of 2022 is in tact. As long as market breadth is strong, expect equity markets to move higher.

Here's the song if you haven't heard it in a while...

___________________________________________________________________________

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.

Comments