War, What Is It Good For?

- Scott Poore

- Mar 6

- 6 min read

Global conflicts aren't good for anyone. It would be best if wars never happened, but that's not feasible in human culture. George Washington once famously said, "My first

wish is to see this plague of mankind, war, banished from the earth." Regardless of the former president's wishes, we're forced to determine what this current conflict means for markets. This week's musings are inspired by the 1970 song "War" by Edwin Starr. Here is some trivia about the song:

This song was released in the Summer of 1970, which was a politically-charged time in the U.S. The song sold more than 500,000 copies (gold status at that time) and reached number 1 on the Billboard charts, staying there for 3 consecutive weeks.

The song was written by Norman Whitfield and Barrett Strong and was originally meant for The Temptations to record. However, Motown executives deemed it too political for their main act.

Edwin Starr stated in 2001 that the song was not about Vietnam, but more about the social wars that were going on in America at the time. It just happened to coincide with the war in Vietnam.

There were two ad-libs by Starr, who added "good God y'all" and "absolutely nothing" while recording the song.

In addition to the song appearing in "Rush Hour" (see video below), it also appeared in many other movies and TV shows over the years, including "Backdraft" (1991), "Teenage Mutant Ninja Turtles" (2016), and "The Wonder Years" (1990).

"War, huh, yeah

What is it good for?

Absolutely nothing, uhh

War, huh, yeah

What is it good for?

Absolutely nothing

Say it again, y'all

War, huh (good God)

What is it good for?

Absolutely nothing, listen to me, oh

War, I despise

'Cause it means destruction of innocent lives

War means tears to thousands of mother's eyes

When their sons go off to fight

And lose their lives"

Here's what we've seen so far this week...

What Is It Good For? Markets have been up and down over the last four trading sessions since the U.S. and Israel began their conflict with Iran. In fact, the S&P 500

Index has closed higher than it opened, but also saw 1-2% intraday swings in at least four of the five trading sessions since the conflict began. That's the price of volatility that wars often create. However, the type of conflict can also matter when it comes to sustained market volatility. Longer conflicts that last multiple years tend to produce negative returns at least 12 months later, by as much as -2% on average. By contrast, shorter conflicts that last only days or months tend to result in positive returns 12 months later, as high as 10% on average.

Whether or not this current conflict stays a "conflict" or becomes a more drawn out war may be more discernable given recent information. According to the New York Times,

there have been some back-channel indications that Iran is interested in pushing away from the table and finding a solution that lead to a truce. That has not been substantiated by the White House, but it is at least a potential sign that the conflict may not drag out. Perhaps the reason for Iran reaching out is the exhaustion of weaponry. The data being tracked shows that missile and drone launches from Iran have steadily declined over the first 8 days of the conflict. Since Day 1 of the conflict both missile and drone launches have decreased 96%. In addition, Bank of America strategist Michael Hartnett has estimated the conflict could be over by the end of this month due to market sentiment and politics. Time will tell how long the current conflict will last.

Meanwhile, the "closure" of the Strait of Hormuz is causing supply disruptions, and not just with regard to oil. The Baltic Dry Index, which we tracked heavily during COVID as

supply dynamics were strained and demand was high, has risen recently after coming back down toward the end of 2025. Since January 15th, the BDI has risen 45% and risen 4% this week alone. The BDI tracks shipments by sea of such goods as iron ore, coal, grains, fertilizers, steel, sugar, and various minerals. Obviously, oil has followed the same path, up 15% since the conflict first started. While Iran cannot technically close the Strait, ships have decided not to travel through the area out of fear and rising shipping insurance costs. The bigger question becomes what affect this will have on inflation. Over the last 3 months, CPI has worked its way down from 3%. If oil continues on its current trajectory and other items shipped through that region of the world are affected, inflation is likely to increase - at least, in the short-term.

Say It Again, Y'all. We've been pretty much pounding the table about the issues surrounding private credit for several weeks. The issues have not been resolved, but

perhaps we're getting some focus on fallout. So far this week, private equity firms such as Apollo, Ares, KKR, and Blackstone have come off the bottom and could be showing signs of stabilizing. However, rising defaults on private loans continue to make headlines.

Bank lending to non-banks and Non-depository Financial Institutions (NDFIs) has reached an all-time high. This is the primary concern moving forward, which is - how

many banks are involved with these private loans and how deep does it go? If these loans comprise only 10% of any major bank's balance sheet, that's one thing. But if it goes much deeper, that is when we could see some type of contagion. Just this week, Blackrock slashed a private loan value to $0 just three weeks after verifying it was worth 100 cents on the dollar. So far, we have not seen anything spill over into the credit space (more on that in a minute) which would indicate perhaps that it's not too much deeper. Markets typically trade ahead of the news, so the fact that these headlines are just now dropping while private equity firms with major private credit liability are starting to move off recent lows could suggest we're getting closer to an end than a beginning for private credit. We'll be monitoring this situation closely over the coming weeks to determine if there more deterioration ahead or if there is any light at the end of the tunnel.

Absolutely Nothing. While conflict and private credit are having their way with markets, the economic picture remains stable. This week, job cuts dropped the most in one month since August of 2022. The previous month, job cuts totaled more than

108,000, but in February cuts dropped by 60,000. That's a trend we would like to see continue for a few months, espcially in light of this month's Jobs Report. Yet, we remain in a "low hire, low fire" labor market environment that is not good over the long-term.

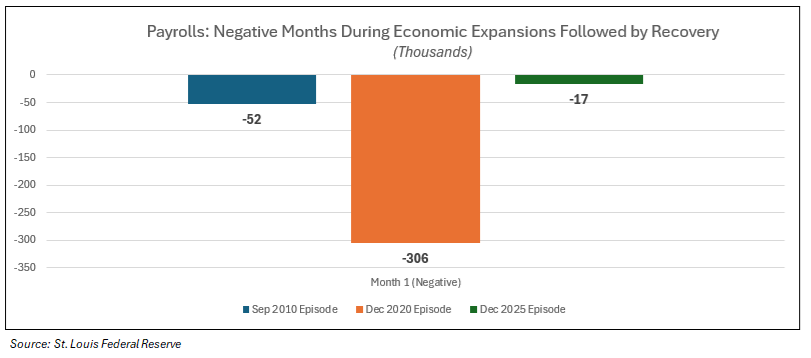

While Jobless Claims remain low and do not indicate the likes of a recession imminent, hiring is not exactly inspiring. This morning's jobs report was a disappointment. The

market had forecast 58,000 jobs to have been added in February, but the number actually came in at -92,000. It's important to note that we have seen negative jobs numbers in one-off months, even during economic expansions. At the beginning of last year, January's jobs number was -48,000, but was followed up by multiple positive months. During the recovery from COVID, December, 2020 was negative -185,000 jobs, followed by multiple positive months. Lastly, September of 2010 saw a negative jobs number of -74,000 only to be followed by three consecutive months with more than 80,000 job gains. While February's number by itself should not cause a panic, we would not want to see multiple negative prints in consecutive months.

As previously stated, we're not yet seeing private credit woes bleed over into public credit. So far, credit spreads remain well below the historical average and are not yet

exhibiting signs of shock. In previous financial crises, the typical rise in credit spreads (difference between safer government bonds and riskier corporate bonds) is 100%, or basically double. Meanwhile, this tends to happen prior to recessions becoming reality and this tends to materialize in 75 days on average. Bear market pundits have been calling for a recession since October of last year and we just haven't seen the signs of credits blowing out that would validate those claims. Things can change, but as we stand here today, current volatility could prove short-term in nature. The proper investment moves for the time being would be to continue reducing concentrations and remain diversified.

Here's a humorous take on the song by Jackie Chan & Chris Tucker...

___________________________________________________________________________

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.

Comments