Jobs Report and Fed Keep Market Guessing

- Scott Poore

- Jul 6

- 3 min read

Markets absorbed a weaker-than-expected Jobs report during the shortened holiday-week. Defensive sectors and “value” stocks out-performed “growth” and momentum

sectors for the 2nd consecutive week. Trading was light last week, as expected, but there was plenty of attention on the Fed and the labor market. In his first international appearance, new Fed Chairman Warsh spoke at the ECB's Forum on Central Banking on Wednesday of last week. He re-affirmed his commitment to little forward guidance, to which markets have still not adjusted.1 He did add that inflation risks had eased in recent weeks as oil has dropped almost 40% since the April 7th peak.2 The decline in oil likely aided AAA in their estimate that holiday travel of the July 4th weekend would exceed last year's number by 0.5%.3

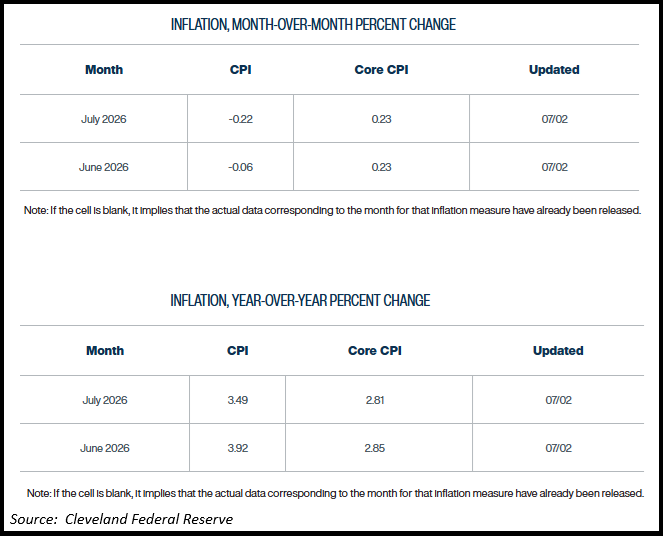

Speaking of inflation, the Cleveland Federal Reserve has once again revised their projections of inflation lower. The June release of the Consumer Price Index has been

revised slightly lower from -0.02% just a week ago to -0.06%. The July forecast is -0.22%.4 If that holds true, that would bring the year-over-year CPI reading at the end of July to 3.49%, which is right at the historical average. If another negative number were to be released in August, it's possible the current market expectation of a rate hike by the Fed would be off the table. The jobs report was weaker than expected in May. Only 57,000 jobs were added versus 114,000 expected.5 A stable or soft job market would lend to the Fed keeping rates steady or cutting. The futures for Fed rates has dropped from an 80% probability of a September rate hike to slightly more than a 65% probability.6 The market will have to keep guessing for another week until the June CPI is released on July 14th.

Market history and the economic backdrop should keep investors engaged for now. From a historical standpoint, when the S&P 500 Index is higher by more than 10% for

the 2nd quarter, it has been higher in every instance in the 4th quarter and higher in all but one instance in the 3rd quarter, going back to 1950.7 The economic data supports more growth in 2026. As measured by the Redbook Sales data, consumers are spending at a rate of +10.5% on a year-over-year basis.8 According to FactSet, more than 55% of S&P 500 companies have provided positive guidance on 2nd quarter earnings and analysts have increased earnings estimates for the 2nd quarter by more than 2%, which is the highest increase in 5 years.9 10 If inflation abates, consumers continue spending, companies grow earnings, and the Fed holds rates steady, the environment could be ripe for markets to grind higher through year-end.

https://aashtojournal.transportation.org/aaa-projects-heavy-travel-over-july-4th-holiday/

https://www.investing.com/economic-calendar/nonfarm-payrolls-227

https://x.com/ryandetrick/status/2072145073123287148?s=12&t=rL12aWyiinzSgh3poyqO0w

https://insight.factset.com/earnings-insight-infographic-q1-2026-by-the-numbers

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.

Comments