Believe It Or Not?

- Scott Poore

- Mar 19

- 7 min read

Updated: Mar 20

The daily volatility we're seeing in markets is something to behold, but it's not as bad as it has been in the past and certainly not as bad as it was during the tariff

announcements last year. It's hard to know where markets are headed sometimes, especially when things are confusing. This week's musings are inspired by the '80s hit TV show "The Greatest American Hero" and it's theme song "Believe It Or Not." Here is some trivia about the show and song:

The pilot episode for the show aired on March 18, 1981. The show was widely popular out of the gate, as the pilot episode was the 4th most watched program that week. Despite popularity waning by the 3rd season and the show ultimately being cancelled, it was nominated for 5 Emmy Awards.

The song was written specifically for the TV show by the duo of Mike Post and Stephen Geyer - who wrote songs for other hit TV shows. Post also wrote the them from "Hill Street Blues" (1981-87) and "The Rockford Files" (1974-80). "Believe It Or Not" climbed all the way to #2 on the Billboard charts and stayed there for 3 consecutive weeks.

The song artist, Joey Scarbury, has some other hits, such as "When She Dances" and "Mixed Up Guy," but "Believe It Or Not" was by far his biggest hit.

The main stars of the show, William Katt and Robert Culp, had difficulties getting along and working with each other. They were able to channel that into the characters and over the course of the series became good friends.

DC Comics tried to sue the producers of the show for copyright violations of their comic hero Superman. The lawsuit was tossed as the premise of the show was actually closer to Green Lantern, who was given a power ring by an alien species to become a superhero.

As a side note, as I was researching the TV show I found out seasons 1-3 are available on Amazon Prime. Enjoy!

"Look at what's happened to me

I can't believe it myself

Suddenly, I'm up on top of the world

It should have been somebody else

Believe it or not, I'm walkin' on air

I never thought I could feel so free

Flyin' away on a wing and a prayer

Who could it be?

Believe it or not, it's just me"

Here's what we've seen so far this week...

Should Be Somebody Else. There are so many things we could kick off this week's musings with, but since the Federal Reserve met this week, that's as good a

place as any to start. As widely expected, the Fed left rates as is, but what was more anticipated was Powell's press conference and the updated economic projections. The Fed's Dot-plot remained unchanged from the previous meeting - i.e., one rate cut in '26 and one cut in '27. However, markets are now forecasting no rate cuts in '26. That would likely depend upon how quickly the conflict in Iran could come to a conclusion.

The Fed Chairman decided to make things interesting on his way out the door. First, the Fed changed their inflation projections from the previous meeting bumping up

PCE from 2.4% in 2026 to 2.7%. Similarly, 2027's projection for PCE was moved up to 2.2% from 2.1% previously. Second, in his usual style, Powell provided little if any real commitments during the Q&A portion of the conference. He stated that long-term inflation expectations are "solid," which runs contrary to the changes in projections. He also stated that the Dot-plot doesn't "bind officials to their projections," so we can basically throw out the current projections? Finally, when asked about his successor, Powell decided to put some doubt into the marketplace by hedging his bets. If, for some strange reason, the Senate doesn't get his successor confirmed, Powell said he would "serve as Chair Pro-tem." He then followed that up by saying he has "no intention of leaving the Fed until the DOJ investigation is over." This doubt hung over the market on Wednesday, so we have Powell to thank for that little going away present.

Look At What's Happened. With all that is going on overseas, its highly likely we will see a spike in the inflation data for March. Since the beginning of March (which is

approximately when the Iranian conflict began) the price of gas has risen from $2.90/gallon to $3.89/gallon. Consumers will feel this pinch when they fill up their gas tanks and that will likely be reflected in the inflation data. The Cleveland Fed is projecting March's CPI number to come in at +0.6% on a month-over-month basis and +3.0% on a year-over-year basis. This would be a substantial increase over the February measurements. If this proves to be a temporary shock, we should see the inflation number come back down relatively quickly with a reduction in oil prices. However, even with a quick resolution in the conflict, it will take some time - maybe months - for oil inventories to adjust.

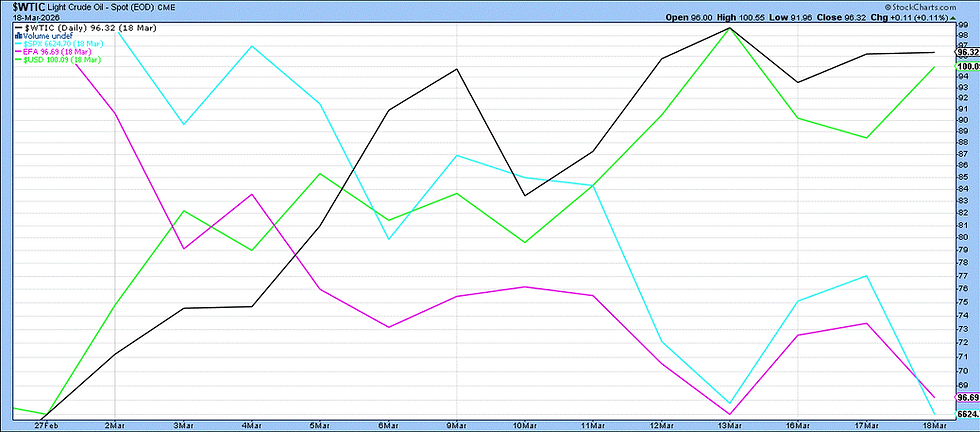

Meanwhile, we are seeing the "risk-off" trade playing out in real time as the movement in risk-off assets (oil and US dollars) and risk-on assets (domestic and

and international equities) remaining contrary. With every headline involving the Iran conflict and oil, equities move lower. However, taking any considerable bets on oil and/or the dollar out-performing over the long-term could be hasty. This week, there has been a turnaround for allies - Japan, Britain, France, Germany, Italy, and the Netherlands - doing a 180 and agreeing to help secure ships navigating the Strait of Hormuz. In addition, the White House has called for Iranian oil already at sea to be "unsanctioned" and free to use on global markets for the 10-14 days worth of supply. Lastly, the President has strongly condemned strikes by Israel on the Pars gas field in Iran, sending a message that escalation is not in the cards for the U.S. military. These revelations have caused oil to trade lower this week. Who knows - the next news item could push oil back above $100/barrel. Placing significant bets on the news item of the day could do more harm to portfolios than good.

Believe It Or Not. Private Credit has continued to struggle with redemptions and questions about financial suitability. That being said, after most private credit has

has seen nothing but red this year, the sector may have reached some stability. Private Credit as a whole is up more than 1% over the last 5 trading days and private equity names that have been heavily exposed to private credit - KKR, Ares, Apollo, Carlyle Group, and Blackstone - are all positive over the same trading period, with some names up more than 5%. Along with those names, the financial sector is trading positive this week for the first time in 4 weeks.

And, just when things are looking a little better for private credit, the prevailing minds in the financial community - Goldman Sachs and J.P. Morgan to name a couple - have

decided in their infinite wisdom to introduce shorting instruments into the market that would allow investors bet against a recovery in private credit. So, a market segment that is already suffering to distinguish signals from the noise is now subject to investors who will find it difficult to differentiate among true private credit firms/funds in this space. One can only hope that these instruments fail to gain much traction or redemptions will pail in comparison to investors getting in line to short the same names.

Not Exactly "A Wing And A Prayer." Despite the pullback in AI, private credit woes, and Iran conflict, the broader economic picture has still not shown the typical signs

of an imminent recession. The two subindices of the Chicago National Financial Conditions Index - Credit and Risk - tend to pinpoint more volatile areas of the economy and usually trigger earlier warning signs than the broader index. Currently, both subindices remain below zero, meaning conditions are loose, and are below the levels seen during Liberation Day last year. By the peak of the tariff-related pullback last year on April 11th, the Credit subindex had risen to 0.18 and the Risk subindex had risen to -0.39. The current level of the Credit subindex is -0.02 and the Risk subindex is at -0.55. An interesting note is that the Credit subindex tends to trigger warning signals about 1 month before the broader index gives off recessionary signals.

Other areas of the economy continued to show life amongst all of the worrisome news. Industrial and Manufacturing Production were higher than expected for the month of

February. Industrial Production was higher for the 4th consecutive month and is up 1.4% year-over-year. Manufacturing Production was higher for the 3rd consecutive month. Redbook Sales continue to be strong (+6.4%), well above the historical average (+4.4%). Initial Jobless Claims came in at 215,000, well below the pre-recessionary levels of +350,000. The news cycle is full of daily activity with regard to the Iranian conflict. Until that eases or we get some kind of ramp down/ceasefire, expect daily volatility to be high. Staying diversified and not making any drastic changes to investment portfolios is probably the best course of action.

Here's the opening to the show that helped shape my childhood...

___________________________________________________________________________

Disclosures

The information contained herein is for informational purposes only and is developed from sources believed to be providing accurate information. The opinions expressed are those of the author, are for general information, and should not be considered a solicitation for the purchase or sale of any security. The decision to review or consider the purchase or sell of any security should not be undertaken without consideration of your personal financial information, investment objectives and risk tolerance with your financial professional.

Forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

Any market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

Past Performance does not guarantee future results.

Comments